MK socks Northwest China's Qinghai Province Photo: VCG" src="https://www.globaltimes.cn/Portals/0/attachment/2024/2024-06-12/f658a75e-0590-4d3c-b6e7-5ad9eeee0740.jpeg" />

MK socks Northwest China's Qinghai Province Photo: VCG" src="https://www.globaltimes.cn/Portals/0/attachment/2024/2024-06-12/f658a75e-0590-4d3c-b6e7-5ad9eeee0740.jpeg" />Mongolian and Tibetan Autonomous Prefecture, Northwest China's Qinghai Province Photo: VCG

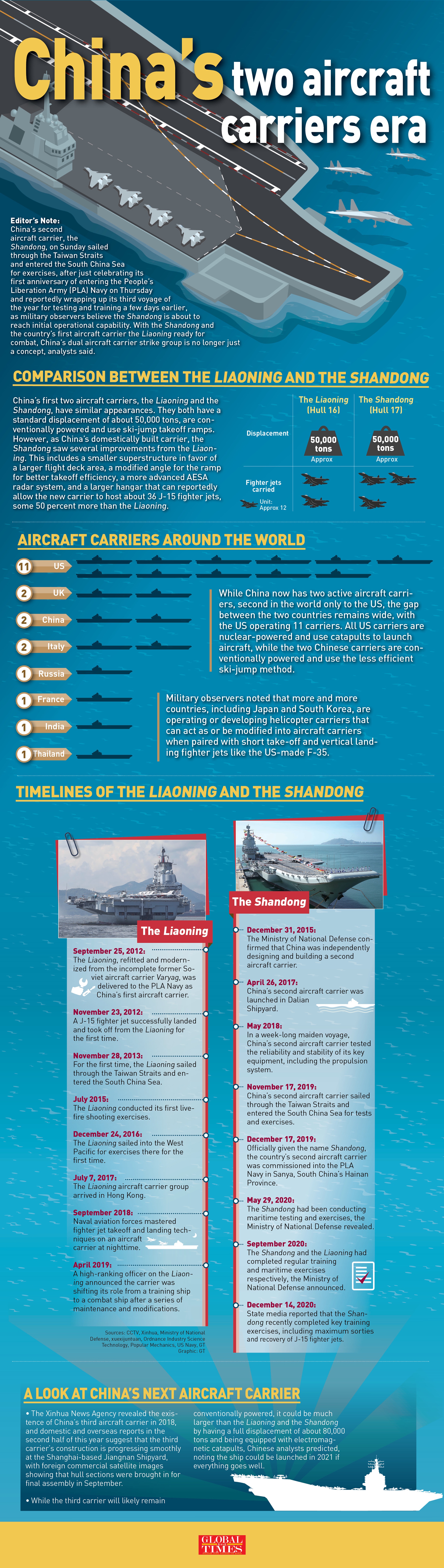

Editor's Note:

As the Chinese economy, along with the global economy, has faced considerable challenges in recent years, some Western officials and media outlets have stepped up their long-standing smear campaign against the world's second-largest economy. They cherry-pick information and distort facts to hype various specious narratives such as "Peak China," while turning a blind eye to China's considerable strengths and vast potential.

As part of the Global Times' multimedia project to set the record straight, the opinion page is publishing a series of in-depth interviews and signed articles with economists, experts and scholars from different countries who share their views on the prospects of the Chinese economy and debunk Western rhetoric. This is the fourth article of the series.

The pattern of world economic development since the beginning of 2024 is clear. International organizations have been consistently revising upward estimates of China's 2024 GDP growth to match the Chinese government's forecast of around 5 percent, with the IMF and Goldman Sachs being the latest to do so. Simultaneously, the US economy has drastically decelerated - official US data shows its GDP growth slowed from 4.9 percent in the third quarter of 2023, to 3.4 percent in the fourth quarter, to only 1.3 percent in 2024's first quarter. The Eurozone is also growing at a stagnant rate.

In parallel with China's much faster economic growth than the US/Eurozone, the Biden administration's recent announcement of 102.5 percent tariffs on imported Chinese EVs, and 50 percent on solar cells, is in reality an admission that the US cannot compete with China in the new green industries that will increasingly power the planet - if the US could compete it wouldn't need tariffs.

China's lead in these new productive forces is even more significant because it is based on a technological advantage, not just the size of the output. As The Economist magazine commented on the Biden administration's tariff announcement: "The real fear about Chinese EVs today is not that they are stealing from America, but that they have left American cars in the dust."

Such facts have now prompted a drastic change in tone in Western economic media from the beginning of the year. Initially, they claimed China's economy was stalling while the US was surging ahead. For example, The Economist magazine in March had stated: "… Uncle Sam is putting the rest of the world to shame. Since the end of 2019, the economy has grown by nearly 8 percent in real terms, more than twice as fast as the euro zone's and ten times as quickly as Japan's."

Even then, this falsified the international economic situation - since the end of 2019, China's economy had grown by over 20 percent, two and a half times as fast as the US. But recent data on China's strong economic performance, and the US slowing, make such claims now look rather ridiculous. Such international media, instead of predicting an economic crash in China, now claim the US and Europe will be overwhelmed by an unstoppable wave of China's green exports.

Understanding why China is enjoying such an economic advantage is obviously crucial to judging whether this will continue. Some analyses focus on features such as the huge scale of China's population, its international dominance in increasingly high-value manufacturing, the rapidly growing education of its labor force, its increasing research and development expenditure, and its explicit adoption of globalization.

These are true, but another fundamental factor ensures China's continuing advantage. China now simply has much more financial resources to invest in new technology than any other country. As China and the US are the world's two largest economies, therefore, the following data compares China and the US, but what is true of comparison of China with the US is therefore even more true of China compared to any smaller economy.

International economic comparisons usually focus on the relative size of GDP - by this measure the US remains the world's largest economy at current exchange rates. But simply comparing the size of GDP is insufficient when it comes to the ability to finance productive investment - particularly in new high-value industries. This is because a huge part of the US economy, 82 percent, is consumed - and consumption, by definition, is not an input into production. So, 82 percent of US GDP cannot be an input into new productive industries.

The result is that China now has by far the world's largest resources to undertake new investment not only as a percentage of its economy but in absolute RMB/dollar terms. But even this greatly understates China's advantage regarding new industries. China's lead in terms of ability to domestically finance its investment, instead of having to rely on inflows of capital from abroad, is larger still.

China's annual domestic generation from all sources of funds available for fixed investment, that is capital creation, on the latest data was $8.2 trillion, almost twice the US' $4.2 trillion. After depreciation, China's finance available for expanding fixed investment was $3.0 trillion, and the US only $0.3 trillion. That is, China's domestic capital creation, the funds available for investment, after taking into account depreciation, is 10 times that of the US.

The result is inevitable. China simply has vastly greater resources available to devote to investment in new industries than any other country. This explains why China, having earlier taken the lead in 5G telecommunications with Huawei, has now taken a global lead in green technology.

US tariffs are powerless to prevent this competitive success by China from spreading to the rest of the world. As the Financial Times recently noted: "Government officials, executives and experts say that the series of new cleantech tariffs issued by Washington and Brussels… will lead to Chinese dominance across the world's most important emerging markets, including Southeast Asia, Latin America and the Middle East, and the remaining Western economies that are less protectionist than the US and Europe."

"That is the part that seems to be lost in this whole discussion of 'can we raise some tariffs and slow down the Chinese advance'? That's only defending your homeland. That's leaving everything else open," says Bill Russo, the former head of Chrysler in Asia.

This reality corrects a misunderstanding regarding innovation. To affect production, innovation cannot remain simply an idea - for example, the introduction of the internet, a truly revolutionary innovation, was not simply an idea but was embodied in a vast network of computers, telecommunications and other investments. Now, China has far greater financial resources for such an investment than any other country. Individual scientists and researchers in China and the US may be equal, but every Chinese scientist or researcher is backed by vastly greater investment resources than in the US.

What has happened with 5G and green technology will inevitably occur in many new industries. China's ability to support its innovation with investment resources, unmatched in any other country, means it will continue to maintain its economic advantage.

The author is Senior Fellow at Chongyang Institute for Financial Studies, Renmin University of China. opinion@globaltimes.com.cn

China lodges solemn representation to US over Taiwan regional official’s reported US visit: FM

China lodges solemn representation to US over Taiwan regional official’s reported US visit: FM ‘Ne Zha 2’ becomes 6th highest

‘Ne Zha 2’ becomes 6th highest China's foreign trade off to a stable start in 2025, as exports hit record high: GAC

China's foreign trade off to a stable start in 2025, as exports hit record high: GAC China to set up national venture capital guidance fund to strengthen innovative firms: NDRC

China to set up national venture capital guidance fund to strengthen innovative firms: NDRC